Start Your Ministry The Right Way

Write your awesome label here.

Course features

-

Author: ZeroPoint University

-

Level: Advanced

-

Study time: 11 hours in total

-

Video time: 61 minutes

-

Exams: 3

More Than A Service

Every Done-For-You Formation Package includes full access to our 508(c)(1)(A) Ministry Formation Course.

While we prepare your ministry documents, you'll gain immediate access to training, templates, and educational resources designed to help you better understand the structure, governance, and operation of your faith-based organization.

Learn while we build.

Study while we prepare.

Launch with confidence.

Done-For-You Formation + Full Course Access

We prepare the documents. You gain the knowledge. Together, we help build the foundation for your ministry.

Custom Documents. Professional Structure. Ready To Use.

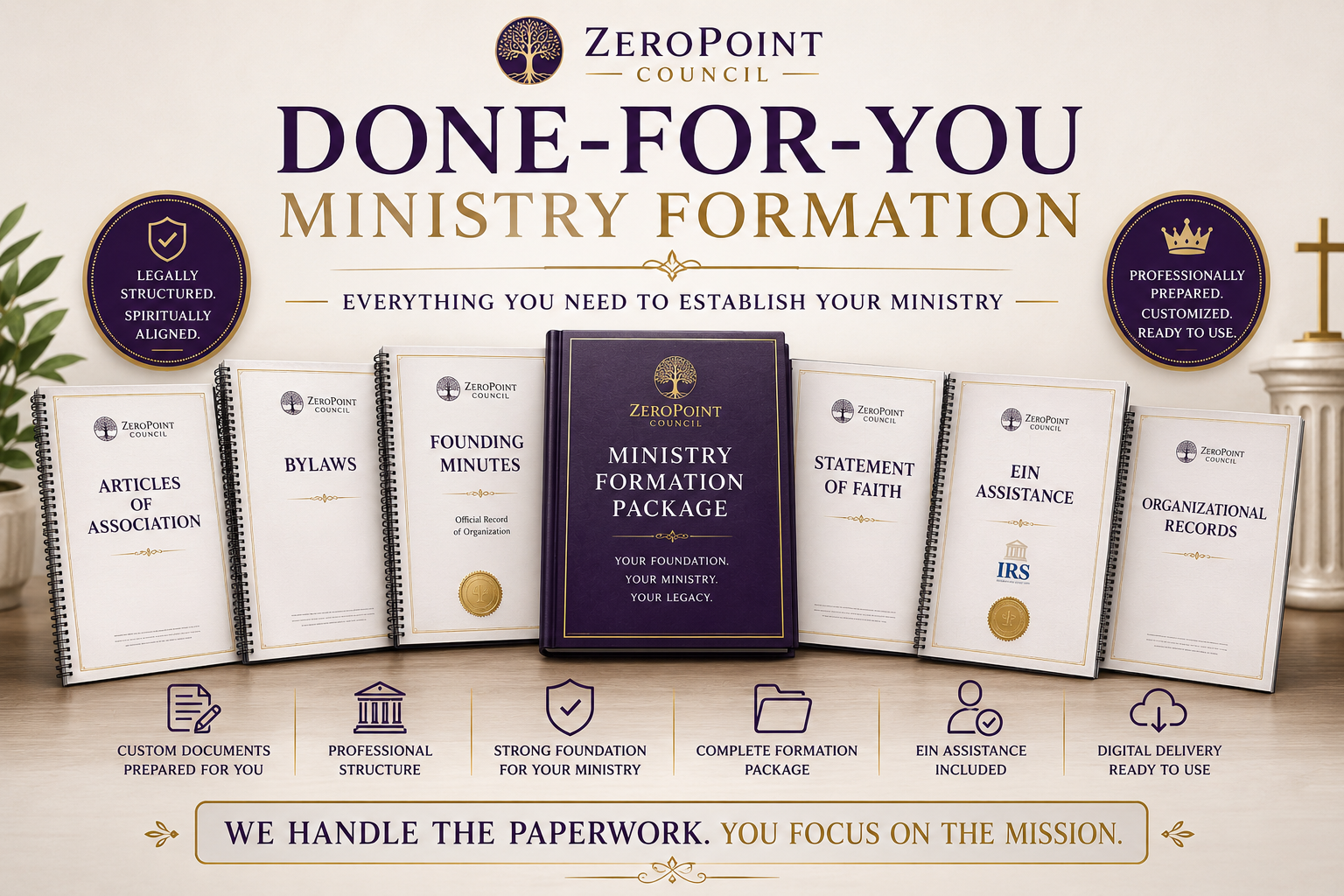

Done-For-You Ministry Formation

Our Done-For-You Ministry Formation Service is designed for those who want a professionally prepared ministry package without spending countless hours researching documents, drafting records, and navigating the formation process alone.

Write your awesome label here.

We Prepare The Documents

✔ No Generic Templates

Write your awesome label here.

We Build The Foundation

✔ No Guesswork

Write your awesome label here.

EIN Assistance Included

✔ No Legal Confusion

Write your awesome label here.

You Focus On The Mission

✔ No Starting From Scratch

Unlock The Complete 508(c)(1)(A) Ministry Formation System

Gain immediate access to the course, downloadable resources, step-by-step training, and community support designed to help you establish and grow your ministry with confidence.

Why This Course?

Control the Terms

What You Will Learn

You’re not forming a church. You’re establishing a Kingdom.

This course gives you the knowledge, resources, and framework needed to build, protect, and grow your ministry with confidence.

This course gives you the knowledge, resources, and framework needed to build, protect, and grow your ministry with confidence.

Write your awesome label here.

What You’ll Get

Every Module Includes

Heaven backs the prepared.

Downloadable Templates (Bylaws, Articles, EIN Letters, Internal Records)

Plug-and-play documents to protect your ministry in law and spirit—built for real-world use, not guesswork.

Real-world Examples and Decision Trees

See how sacred structure looks in action—then choose your own path with confidence and clarity.

Custom Checklists & Trackers

Stay organized, stay sovereign—know what to do, when to do it, and how to do it legally.

Legally Sound Fill-in-the-Blank PDFs

Every document is pre-framed, professionally written, and easy to complete—no law degree required.

Laws & Doctrines Cited for Every Lesson

We don’t just tell you what to do—we show you the law behind every move so you’re never left unarmed.

Video Lessons, Reflections & Quizzes

Each video builds your mastery. Each reflection grounds your vision. Each quiz reinforces your knowledge.

Bonus Materials

Clergy Legal Rights Summary Sheet

A quick-reference document for understanding your protections under federal, state, and international law—carry it, quote it, stand on it.

LEARN more

“Tools for Sovereign Ministry Implementation” PDF Bundle

Your tactical kit: forms, templates, and frameworks to establish, fortify, and operate with divine precision.

LEARN more

Certificate of Completion

Proof you didn’t just study the path—you walked it, claimed it, and are ready to lead.

LEARN more

Referral & Affiliate Opportunities to Earn

Spread the truth, grow the mission—get rewarded for being a voice in the movement.

LEARN more

Access to ZeroPoint Council for support

You’re not doing this alone. Get guidance, legal insight, and spiritual reinforcement from a higher order.

LEARN more

ZeroPoint Ministry Roadmap PDF

A high-level blueprint guiding your first 90 days—from foundation to full operation, without confusion or compromise.

LEARN more

This Is More Than a Course — It’s Activation

You’re not just learning policies—you’re reclaiming power. This is your initiation into lawful ministry, spiritual governance, and kingdom building.

You were called to this — not by man, but by Divine Order.

This isn’t just paperwork. It’s a heavenly assignment with lawful authority on Earth.

This is your chance to build something eternal, protected, and set apart.

This isn’t just paperwork. It’s a heavenly assignment with lawful authority on Earth.

This is your chance to build something eternal, protected, and set apart.

FAQs for How To Set-Up A Tax Exempt 508(C)(1)(A), Faith Based Organization

What is included in the Done-For-You Ministry Formation Service?

We prepare the foundational ministry formation package for you, including organizational documents, governing records, ministry structure documents, and supporting records designed to help establish your faith-based organization. You receive professionally prepared documents delivered digitally, along with guidance on implementation.

Do I have to complete the documents myself?

No. This is a Done-For-You service. We handle the preparation of the formation documents so you don't have to start from scratch or rely on generic templates.

Are the documents customized to my ministry?

Yes. Your documents are prepared using the information you provide about your ministry, mission, leadership structure, and organizational goals.

Is EIN assistance included?

Yes. We provide guidance and assistance with the EIN application process. The ministry's responsible party remains the applicant, but we help ensure the process is completed properly.

How long does the process take?

Most ministry formation packages are completed within a few business days after all required information has been submitted. Processing times may vary depending on the complexity of the ministry structure and responsiveness during onboarding.

Is this the same as a 501(c)(3)?

No. This service is designed for faith-based organizations operating under 508(c)(1)(A). We encourage all clients to conduct their own research and consult qualified professionals regarding tax matters and organizational decisions.

Can I use this for a church, ministry, outreach, or faith-based organization?

Yes. This service may be appropriate for churches, ministries, religious societies, faith-based educational organizations, outreach programs, and other organizations established for religious purposes.

What happens after I place my order?

After purchase, you will receive an onboarding questionnaire requesting information about your ministry. Once submitted, we begin preparing your formation package and provide updates throughout the process.

Will I receive physical documents?

Unless otherwise specified, all documents are delivered electronically in digital format, allowing you to download, store, and print your records as needed.

Unless otherwise specified, all documents are delivered electronically in digital format, allowing you to download, store, and print your records as needed.

Do I receive support after my documents are delivered?

Yes. We provide follow-up guidance to help you understand your formation package, organizational records, and next steps after delivery.

Do I need prior experience with ministry formation?

No. Whether you're starting a new ministry or restructuring an existing organization, the service is designed to simplify the process and provide a professionally organized foundation.

What makes this service different from other ministry formation services?

Most services provide generic templates and leave the rest to you. We prepare your ministry formation package using the information you provide, helping you establish a properly documented faith-based organization without spending countless hours trying to figure everything out yourself.

Is this service only for churches?

No. This service can be used for churches, ministries, faith-based organizations, outreach programs, educational ministries, healing ministries, and other religious organizations established for spiritual purposes.

Do I need to be ordained before starting?

No. You do not need to be ordained before purchasing this service. We can assist with ministry structuring and provide supporting organizational documents as part of the formation process.

What documents are included?

Your package may include Articles of Association, Bylaws, Founding Minutes, Statement of Faith, Ministerial Appointment Documents, Organizational Records, and other supporting formation documents depending on your ministry's needs.

Can you help if I already have an existing ministry?

Absolutely. Whether you are starting a new ministry or updating an existing organization, we can help organize and document your ministry structure properly.

Does this course include templates and legal documents?

Absolutely. One of the most valuable parts of this course is access to a comprehensive ministry formation document library.

You'll receive downloadable templates, sample organizational records, ministry governance documents, founding records, statements of faith, bylaws, ministerial appointment documents, and other resources designed to help you establish and maintain a well-documented faith-based organization.

Rather than forcing you to start from a blank page, we've provided practical tools and examples that can help simplify the formation process and save you countless hours of research and drafting.

What happens after I finish the course?

By the time you complete the course, you'll have a clear understanding of how faith-based organizations are structured, documented, and managed. You'll know how the various formation documents work together, how to maintain organizational records, and how to build a strong foundation for your ministry's future.

More importantly, you'll leave with practical tools, downloadable resources, and a step-by-step framework that you can continue using as your ministry grows.

This isn't just information—it's a blueprint designed to help you move from uncertainty to implementation with confidence.

Our students love us

Enroll Now

Build in truth, backed by law, and activated by purpose.

Build What They Can’t Tear Down

WHO DOESN'T LIKE FREE?

EXPLORE A RANGE OF AMAZING FREE COURSES

Check out the latest from our blog

Created with